The first grant recipients of a £775m fund were revealed last month, but what is the alternative remedies package, and why is it handing out money to UK banks?

Canary Wharf, London was at the centre of the 2008 UK financial crisis (Credit: David Iliff via Wikipedia)

A £280m grant was recently shared between three UK challenger banks to boost their business banking operations – the source of which was the lesser-known alternative remedies package.

Metro Bank took the largest proportion with £120m, while mobile bank Starling pocketed £100m and ClearBank – in partnership with business bank Tide – received £60m.

What is the alternative remedies package?

It was the first allocation of funds from the alternative remedies package money pot, which was created as a convoluted by-product of the UK government’s bail-out of the Royal Bank of Scotland (RBS) during the height of the 2008 financial crisis.

The fund is an EU-prescribed initiative designed to foster competition in the UK SME financial services market, and ensure that RBS does not gain an unfair advantage from its state aid rescue a decade ago.

It’s implementation is being overseen by the specifically-created independent body Banking Competition Remedies (BCR), which is being headed by Lord Godfrey Cromwell.

In a statement on the UK government website, it explains: “The alternative remedies package is designed to improve competition in the UK business banking market, addressing the market distortions resulting from the provision of state support to RBS, and to resolve RBS’ state aid commitments.”

In total, the alternative remedies package will inject £775m into the UK banking industry via two separate schemes throughout the year, with the aim of diversifying the business banking landscape and encouraging customer mobility away from RBS assets.

What is the history of the alternative remedies package?

When EU lawmakers approved the UK government bailout of RBS in the fallout of the financial crisis, they did so with the provision that the bank would divest part of its SME banking services.

The idea was for the bank to sell off its Williams & Glyn division as a standalone entity, which would have included a network of hundreds of branches serving more than 250,000 SME customers.

This plan was later abandoned, however, after it was decided Williams & Glyn would be unviable as an independent venture.

A substitute arrangement was sanctioned by the EU Commission in 2017 for RBS to retain the Williams & Glyn assets, and instead create a £775m fund – the alternative remedies package – to be used to boost competition in UK SME banking industry and help other banks challenge RBS in that space.

How does the alternative remedies package work?

The alternative remedies package consists of two separate initiatives – the incentivised switching scheme, and the capability and innovation fund.

The former allocates up to £275m for challenger banks to use as incentives to encourage SME customers of Williams & Glyn switch their accounts away from the RBS business – with a further £75m made available by the bank to cover customers’ switching costs.

The capability and innovation fund is a £425m reserve that will be granted in stages to eligible challenger banks to help develop and improve their capacity to compete in providing banking services to SMEs, and improve the quality of the financial products they are able to offer business customers.

This was the source of the £280m allocated last month to Metro, Starling and a partnership between ClearBank and Tide in what was the first, and biggest, of four planned rounds of funding.

Responding to the grants last month, Federation of Small Businesses national chairman Mike Cherry said: “It’s a relief to see this funding is now finally being handed out after a lengthy application process.

“For too long, the small business banking market has been dogged by lack of competition and poor customer service.

“Properly used, the alternative remedies package will go some way to addressing these challenges.

“These sizeable sums must be put to good use. Where grants are being handed to well-established players – particularly those under financial pressure – BCR needs to step-up its scrutiny.

“What we can’t have is a situation where this funding is swallowed up by day-to-day operations, rather than fully dedicated to improving small business offerings.

“The commitment to spending a portion of this allocation on expanding the UK’s branch network is welcome.

“In-person support and cash deposit facilities are hugely valued by thousands of small business owners, especially those based in rural areas.”

Who benefits from the alternative remedies package?

The goal of the alternative remedies package is to promote competition in the UK’s SME banking sector – ultimately improving the prospects of challenger banks looking to give business customers an alternative to RBS, while also making switching to a new account provider a more appealing prospect for small enterprises.

Account switching in the UK is generally low among small businesses, despite incentive schemes such as the Current Account Switch Service (CASS), which was launched in 2013 to encouraging people and firms to be more flexible.

Figures from Bacs, the payments organisation run by Pay.UK and tasked with operating CASS, show that while the scheme has attracted decent numbers – between 60,000 and 100,000 switches per month during 2018 – the vast majority of these have been for personal accounts.

Business bank switching accounted for between only 2.5% to 4% of all monthly account switches throughout 2018, with similar levels posted for 2017 and the first two months of 2019.

The incentivised switching scheme only launched officially last month, with nine banks initially selected for immediate inclusion, so its impact will be interesting to monitor.

Challenger banks receiving grants obviously benefit from a significant capital injection to sustain business growth, and, in theory, banking customers should benefit from the positive effects of better-funded rivals making the industry more competitive with superior products and services.

The capability and innovation fund – Pool A winners

The first round of financing from the capability and innovation fund awarded the three largest individual grants available, with recipients Metro Bank, Starling and ClearBank/Tide able to use that capital boost to improve their standing within the market.

Metro, which pocketed £120m from the fund, plans to use the new capital to drive the expansion of its bank branch network across the UK – a unique strategy among its peers, which are largely reducing branch numbers.

CEO Craig Donaldson said: “Securing this award allows us to accelerate our plans to revolutionise banking for SMEs.

“It will help us bring much needed competition to the underserved SME hotspots in the north, while investing in our digital capabilities and creating new jobs.

“We already provide tens of thousands of businesses with market-leading service and convenience, and these funds will enable us to introduce new services and products for more SME customers across the country.”

The decision to award Metro the biggest available prize raised eyebrows in some quarters, given the high-profile struggles the firm has experienced this year – with an “accounting error” in its end of year results causing share prices to plummet dramatically and prompt a regulatory investigation.

Digital challenger Starling, meanwhile, was awarded £100m to develop its business banking products, which it launched last year, and has pledged to match the grant with £95m of its own money.

Starling has made a big impact since its launch as an open banking disruptor, proving a hit with customers and winning top honours at the British Bank Awards for two years in a row.

CEO Anne Boden said: “Starling Bank is delighted to have received this award. It will accelerate our ability to reshape the SME banking market.

“Starling will deliver an advanced, fully-digital offering that connects SMEs with the financial solutions they need to thrive.

“This is the opportunity to bring new technology and a new approach to the sector.”

The remainder of Pool A funding went to a partnership between ClearBank – a digital clearing bank – and business-focused challenger bank Tide.

The two companies will work together using technology innovation to bring disruption to SME banking, and plan to match the grant with investment of their own in a bid to capture a “substantial share” of a UK market that has been “failed” by a longstanding oligopoly.

What’s next for the alternative remedies package?

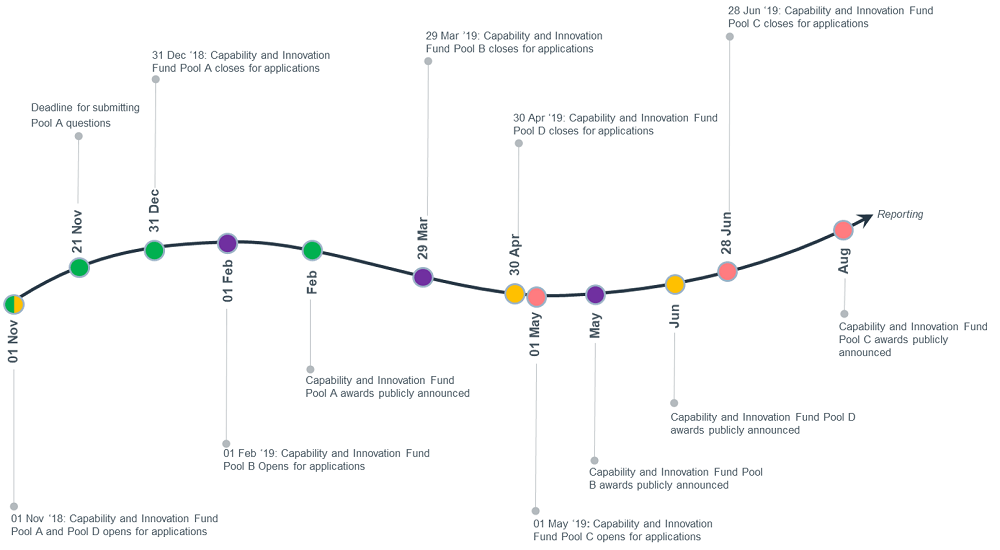

With the wheels of the alternative remedies package now well in motion, and the first grant allocations having been handed out, it is worth noting some of the key upcoming dates to keep an eye on.

The incentivised switching scheme was officially launched on 25 February, with nine organisations included in the first round of applications – with a further two to be added pending confirmation.

A second application window for eligible banks to be added to the funding scheme will be opened in June, with confirmation of successful entries expected later in August.

The switching incentive initiative is planned to run for an initial 18 months, or until the full £275m reserve has been distributed among the chosen organisations.

For the money still available via the capability and innovation fund, applications for Pool B – which focuses on helping firms either modernise a legacy business banking product, or launch a brand new product – are currently being accepted, with a deadline set for March 29.

Two grants of £15m are up for grabs in this category, as well as one of £50m.

Entries for Pool C – which includes four individual grants of £10m for improving the process of making payments and lending – opens on May 1, with submissions accepted until June 28.

Pool D has five grants of £5m available and is open to banks broadly looking to commercialise financial technology.

Applications for this category have been open since since November last year, and will close on April 30.